Momentum strategies

Haven’t posted anything in ages, so here’s a quick hack I threw together in Python on a Sunday night. Basically I wanted to know whether momentum strategies work well for international stock indexes. I spent a bit of time putting together a strategy that buys the stock index if the return during the previous n days was positive, otherwise doesn’t do anything. I ran this strategy for a basket of approximately 20 stock markets.

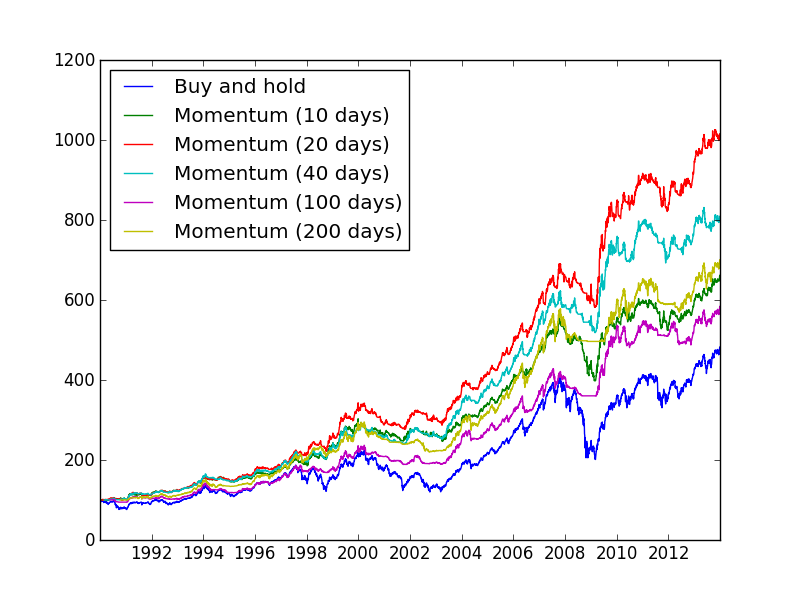

Anyway, disregarding transaction costs, yada yada, historical returns are not a guarantee for future returns, blah blah, here are the results. It doesn’t matter which window size we use, we still make a little bit more money from a momentum strategy:

Returns for each strategy. Click picture to see source code

Returns for each strategy. Click picture to see source code

Minor note: the returns above ignore volatility, actually understating the impact. Looking at Sharpe ratios instead, the momentum strategies have ratios between 1.08-1.40, whereas the “Buy and Hold” strategy has a Sharpe ratio of 0.49.

This whole exercise was mostly for fun, but it was a delight how easy it was. I just installed ystockquote and was able to put everything together within an hour. I’ve worked in finance, where this was almost harder to do. With such a low barrier, I almost consider it a duty for any hacker with a trading account to spend some time hacking on their finances. I will certainly spend more time analyzing my trades. Not necessarily engaging in anything crazy though, and I certainly discourage anyone from doing so.